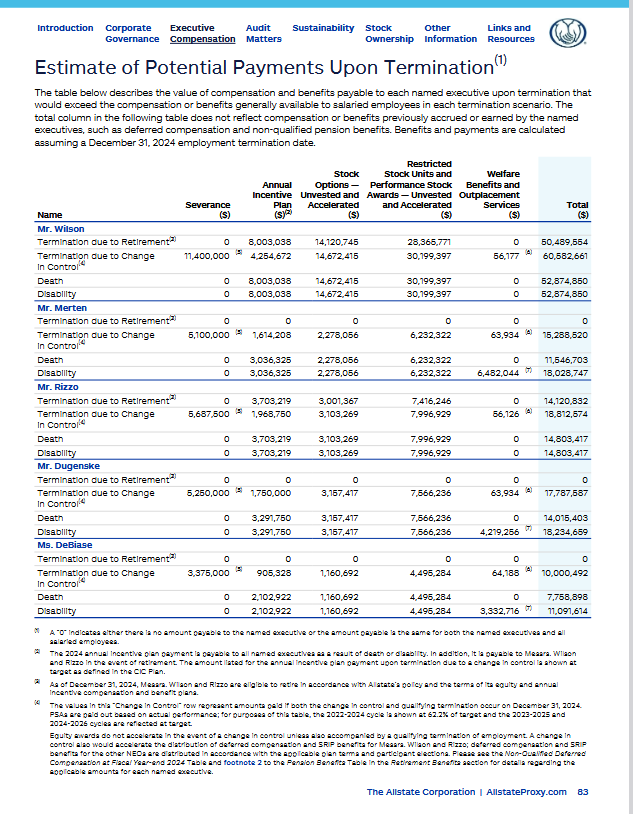

Item 402(j) of Regulation S-K provides a lot of flexibility when companies make their “Potential Payments Upon Termination or Change-in-Control” disclosure. In requiring information about potential payments to NEOs in connection with certain specified terminations of employment or a change in control, the SEC allows companies to provide the disclosure in either a tabular or narrative format (most companies opt to use tables). And if its tabular, companies are free to devise their own.

The result is that the look of disclosures are all over the map in this area. Some more easy to read than others. And some companies provide a disclaimer that their estimates are indeed that, an estimate – and some don’t. It’s a good thing to provide.

In its 2025 proxy statement, Allstate does a nice job with its Item 402(j) table: