The SEC’s 2023 insider trading rules require not only disclosure about Rule 10b5-1 trading arrangements and grants of option awards within four days of reporting material nonpublic information, but also annual disclosure about policies and practices related to the timing of option award grants and release of material nonpublic information.

While the latter is not a new requirement in principle, CD&A discussion usually focused on the timing and pricing of specific grants or was embedded in the compensation committee’s decision-making timeline. With the new Item 402(x) of Regulation S-K now in effect, we expect more companies will choose to include a separate section dedicated to its equity grant timing practices (irrespective of whether options are currently part of the equity mix).

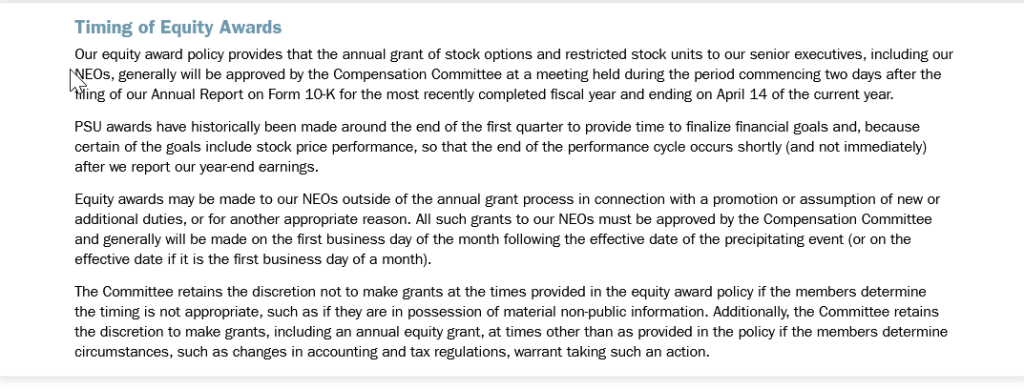

Here’s an example from the 2024 Freeport McMoRan proxy:

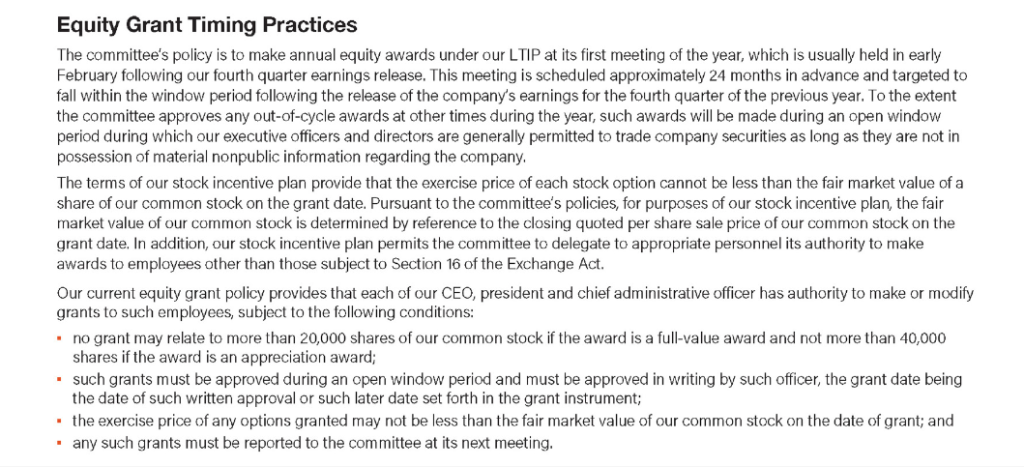

And here’s an example from the 2024 PVH Corp proxy: