It might well be the case that many of you reading this don’t have any input into the IR web page at your company (or for your clients). When I was in-house, drafting the disclosure documents filed with the SEC, I had nothing to do with the company’s IR web page. Maybe that should change.

If you peruse our set of 25 criteria that companies can use to make their IR websites more transparent, one theme comes through loud and clear: the “Accessibility” Pillar is key. The investor relations web page should be easy to find from a company’s home page – and from a Google search. And then the items you have posted on your IR web page should be easy to find on that page – and from a Google search (my next IR web page blog is about SEO and search results).

This is common sense. Studies show that people have little patience to find what they want when they go searching online. A fraction of a second could mean the difference between someone sticking with the search or moving on. Maybe you don’t care too much whether investor and other stakeholders can find your content easily, but you should.

I could go through our list of 25 criteria but they do all emanate from the bottom line is how quickly can someone find something. Is your IR web page nicely organized and easily accessible?

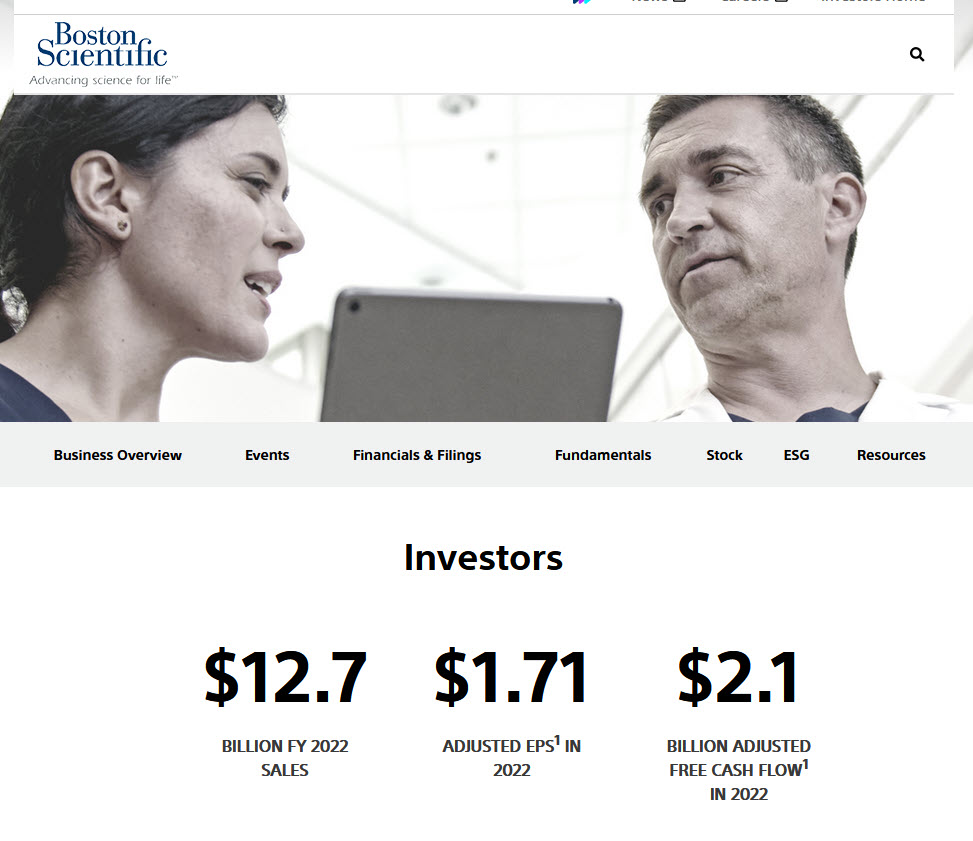

For an example of who does it well, you don’t have to look far – as Boston Scientific’s IR web page won the top prize in the “Best IR Web Page” category in the 2023 Transparency Awards. Second place was Altria’s IR web page – and third place was Allstate’s IR web page. Check them all out…