Following up on my recent blog about the “CD&A Executive Summary,” understanding the elements of a compensation program are so crucial that a good proxy summarizes this information at the outset. A reader wants to know what your elements are, how they are structured to work together to achieve the company’s compensation objectives – and whether they worked as intended. As part of this, disclosure should be made about the purpose of each element, and also include key terms and conditions of variable compensation components.

Transparency Criteria #53 for the proxy states:

Pay mix and applicable components of director compensation (including all committee chair retainers and equity awards) are disclosed in a matrix, table graphic or using other visual elements.

Location of the Disclosure Flexible

Many companies include this elements summary as part of their proxy summary and that is fine. Other companies include it as part of their CD&A summary and that might work a little better because it helps sets the table for the rest of the compensation discussion.

Disclose the Objective and Purpose of Each Element

It’s important to go beyond merely listing each element and start getting into why the compensation committee choose it. Readers want to know the “why” and learn about the purpose and objective of each element.

They also want to know some details about the metrics for your incentive programs. And the weighting of those metrics. The vesting periods. All of this should be neatly wrapped into a table or graphic so that a reader can get a good sense of what the comp program looks like at a glance.

Here is a great example from Mondelez’ 2023 proxy (page 69) based on its simplicity:

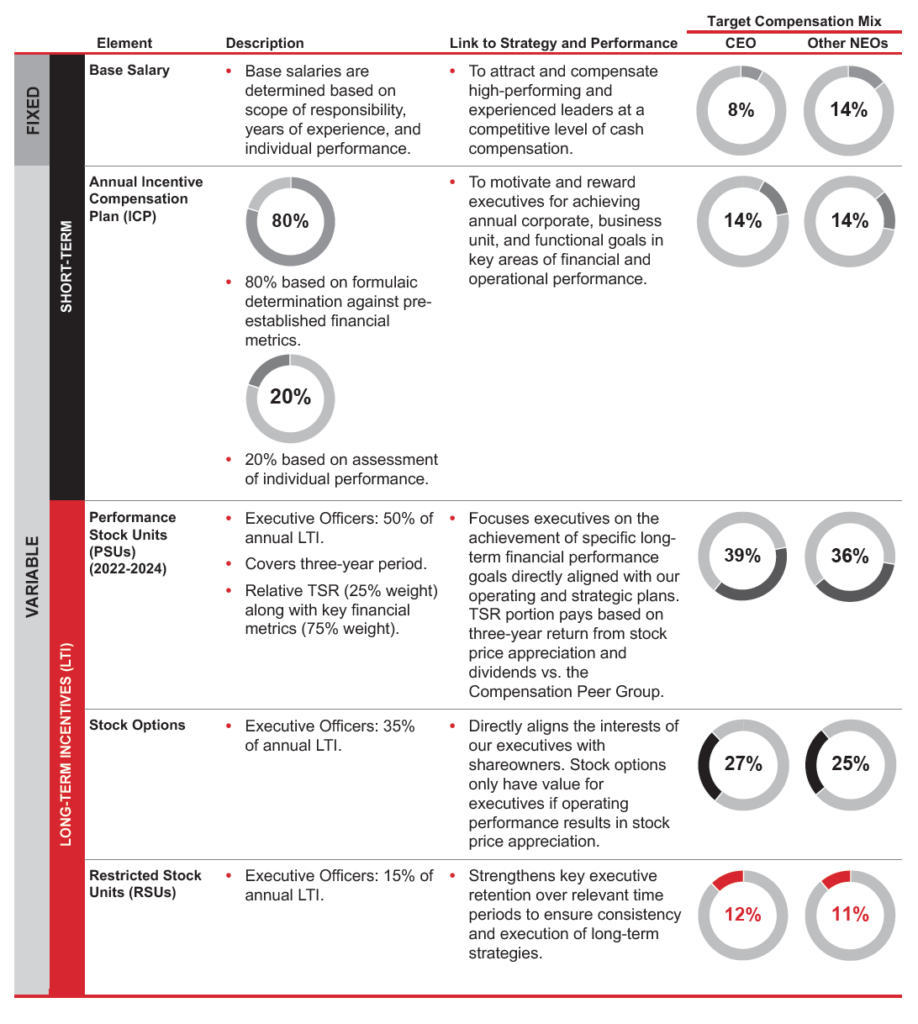

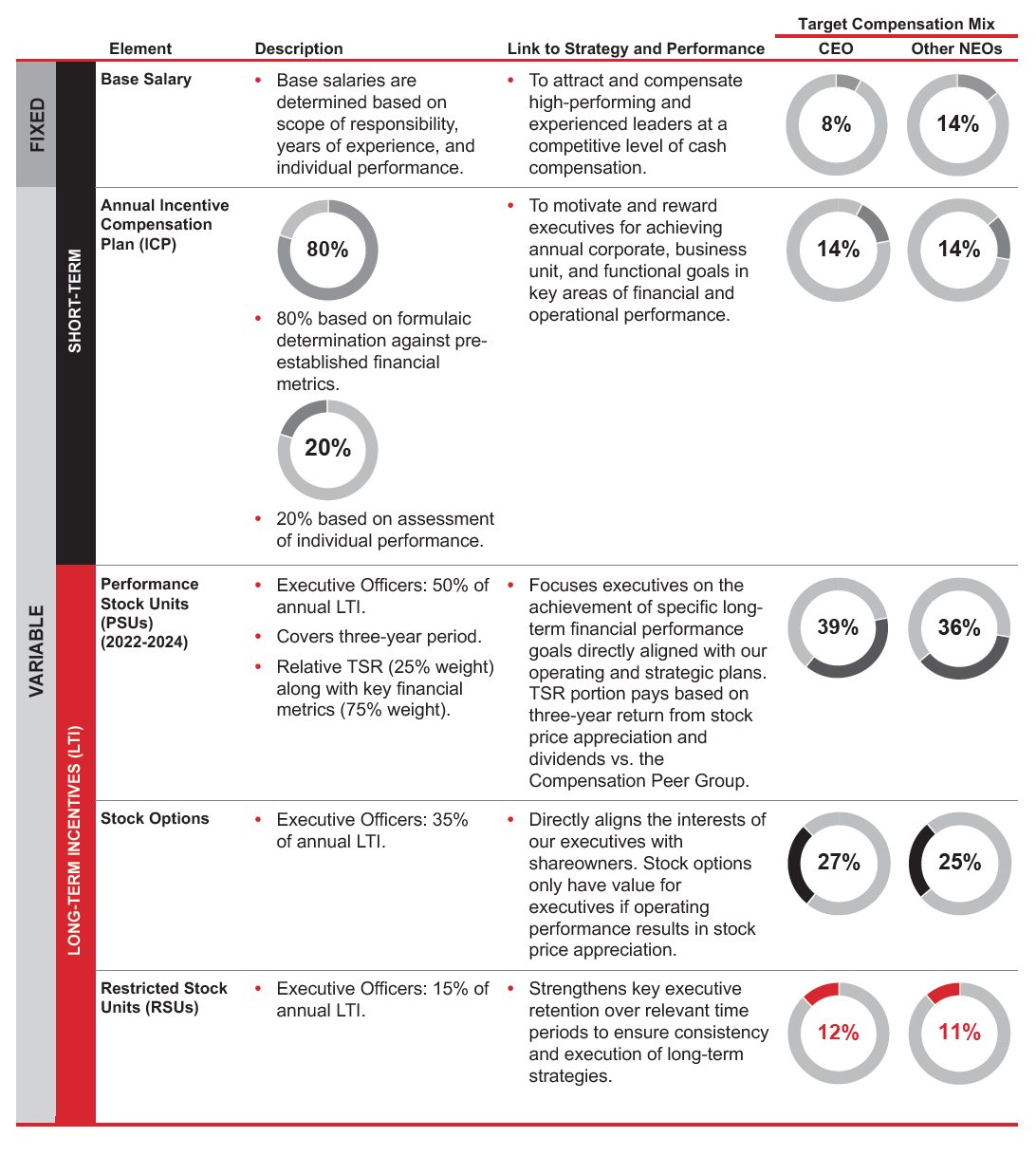

And dig this example from Honeywell’s 2023 proxy (page 66), which includes the pay mix with more detail on the important aspect of “why”: