Transparency Criteria #18 for the proxy states:

The proxy summary or introduction to election of directors proposal includes a board summary matrix, table, graphics, or other visual elements that names all directors and includes, at a minimum: each director’s primary occupation; age; independence; tenure; and committee membership.

There is a two-fold rationale for having a board summary table. First, it helps a reader with digesting voluminous content. Proxies these days contain so much information about the board – understandable given that one of the primary purposes of the proxy is to give shareholders information so they can make an informed choice when electing directors at the annual meeting – that having a summary of that disclosure is prudent.

Second, it allows the reader to scan the summary and get a good sense of what this particular company is doing with its board. Most shareholders don’t really evaluate a company’s board individual by individual. Rather, they analyze the board as a whole.

A snapshot like the board summary table gives readers the opportunity to do that more quickly than slugging through 30-odd pages of disclosure. They can get an answer to the questions: “Does this board feel right? Is there a sense of balance in its composition from the variety of perspectives we view boards as needing as stated in our voting guidelines (e.g.. skills, expertise, demographics)?”

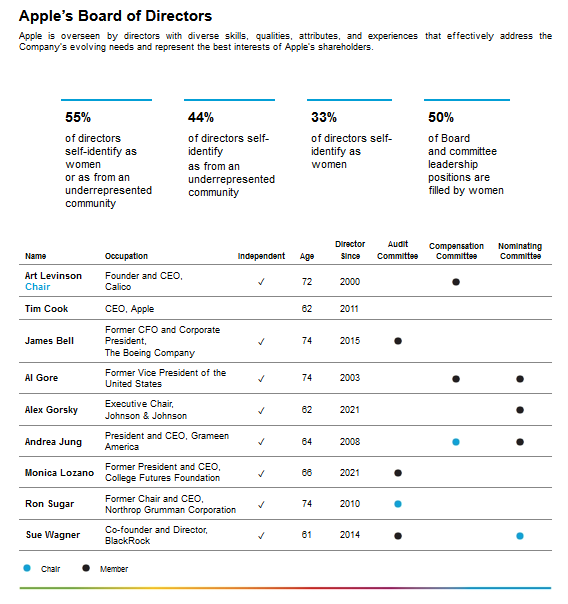

Apple’s proxy provides a good example of a nice simple board summary table (on page 12):

Southern Company’s proxy provides a board summary table in another nice visual format (on pages 20-21):