Over the years, I’ve talked to a number of brilliant in-house disclosure drafters and a number of them have said that they go through the exercise of re-imaging a section in their proxy or 10-K that feels stale. Perhaps it’s a five-year check. And that all sounds good on paper, but in practice I wondered if it was possible given the pace of regulatory, stakeholder and world changes that makes our lives so unbearably busy. “Yeah, that sounds good but…”

Then I came across the CD&A for the 2024 Murphy Oil Corporation proxy (starting on page 18) and I am proved wrong. In comparing the 2023 proxy (starting on page 20) to this year, it’s clear that they started from a blank sheet of paper, stripped out every boilerplate phrase and flabby paragraph, and put the rest into a Q&A format. It’s cool. And note that the ’23 proxy wasn’t bad at all – but the company still decided to revamp it for more transparency.

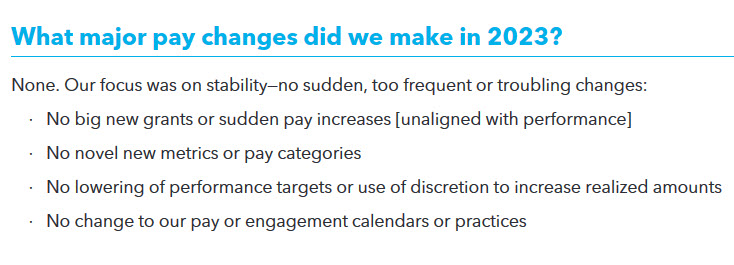

Here’s a snippet: