As noted in this report from Labrador, for companies with low say-on-pay votes, it’s important that disclosures related to outreach and responsiveness are easy to locate. Labrador recommends that companies hit the highlights of their responsiveness in the Proxy Summary with a cross-reference to a standalone engagement section in the CD&A, apart from their normal engagement disclosures in corporate governance.

Many companies also disclose highlights related to their compensation engagements in their letters from the compensation committee (at the start of CD&A) and letters from board leadership (at the start of the proxy). Well-designed graphic elements are also critical to easily show the breadth of engagement and response to feedback as well as other key aspects of program design, including its link to company strategy and performance.

Elements to consider for the Proxy Summary, as appropriate:

- The breadth and scope of the business (background about the company)

- Business highlights (not necessarily specifically tied to compensation metrics, although financial and non-financial results tied to compensation metrics should be included)

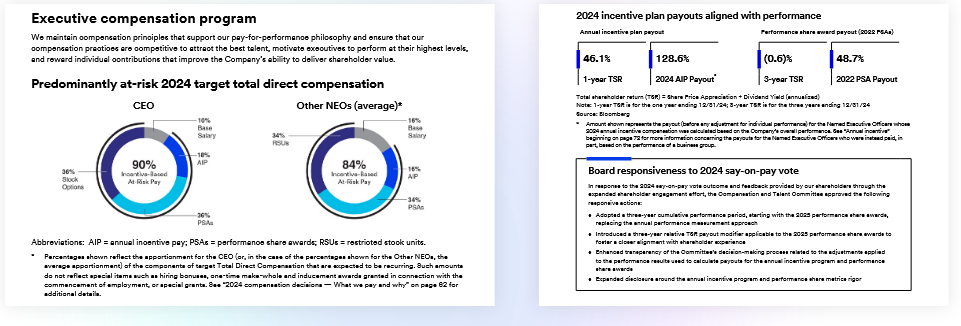

- Compensation elements and their metrics

- Pay for performance alignment over time – with the performance metric(s) that is most relevant for the company and its industry

- Compensation governance (“what we do / don’t do”)

- Shareholder outreach and a summary of resultant changes

There are a number of disclosure examples in the report, including this disclosure from 3M: